R.A. 10963 or the TRAIN Law amended 72 provisions of the National Internal Revenue Code of 1997, inserted eight subsections (Section 51-A, 148-A, 150-A, 150-B, 237-A, 264-A, 264-B, 265-A), repealed three provisions (Sections 35, 62 and 89) and deleted 9 paragraphs of the NIRC of 1997 and the most significant changes are as follows:

Overview of the Amendments in the Tax Code

1). The Expansion and Strengthening of Certain Powers of the Commissioner of Internal Revenue (CIR) and BIR officials:

- On the power to examine returns – The Cooperative Development Authority is required to submit to the BIR a report on tax incentives enjoyed by registered cooperatives pursuant to the TRAIN Law and “The Tax Incentives Management and Transparency Act (TIMTA)” or R.A. 10708 of 2015 [Section 5(B) as amended].

- The CIR can examine returns and make assessment notwithstanding any law requiring prior authorization of any government agency or instrumentality [Section 6(A) as amended].

- New power to conduct periodic random field tests and confirmatory tests on fuel required to be marked in warehouses, storage tanks, gas stations, and other retail outlets [Sections 148-A and 171 as amended].

2). The Limitation of Certain Powers of the CIR and BIR Officials:

- Limitation on the power to prescribe real property values – The CIR must now conduct mandatory consultation with the public and private sectors in the exercise of the power to prescribe real property values or zonal values. No adjustment in zonal valuation shall be valid unless published and posted in public places [Section 6(E) as amended].

- Deliberate inaction on application for refund of VAT input tax credits is now prohibited and punishable as an offense – The BIR can no longer neglect or refuse to act on applications for tax refund which must be processed within the shorter period of 90 days (previously 120 days). Deliberate inaction of the BIR on requests for refund is now punishable [Section 269(j)].

- The power of the CIR to prescribe intervals for filing returns and the manner or time of payment of percentage taxes other than the time provided in the Code has been deleted from Section 128.

3). Imposition of New Tax Rates on the following:

- Income tax of individual taxpayers [Section 24(A) as amended]

- Final income tax from interest income derived from foreign currency deposits by resident individual taxpayers [Section 24(A) as amended] and domestic corporations [Section 27(D)(1) as amended]

- Final income tax on cash and/or property dividends by individuals [Section 24(A) as amended] and domestic corporations [Section 27(D)(2) as amended]

- Final income tax from capital gains from sale of shares of stock not traded in the Stock Exchange [Section 24(A) as amended]

- Fringe benefit tax [Section 33(A) as amended]

- Estate tax [Section 84 as amended]

- Donor’s tax [Section 99(A) as amended]

- Stock transaction tax [Section 127(A) as amended]

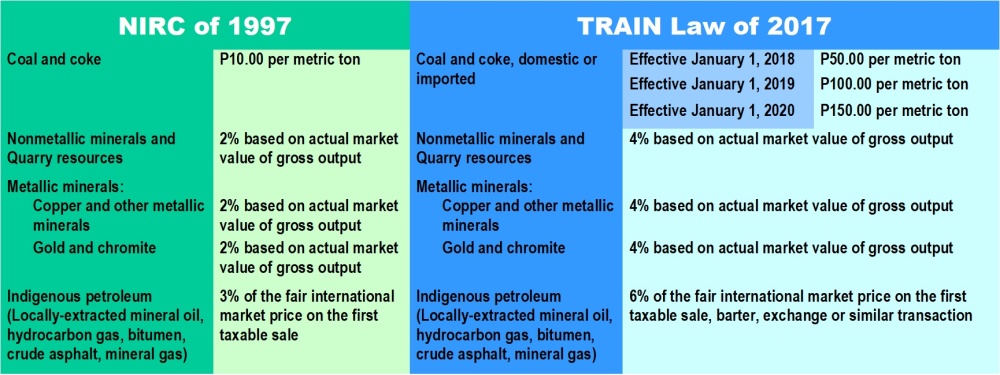

- Excise taxes [Sections 145, 148, 149, 151, as amended]

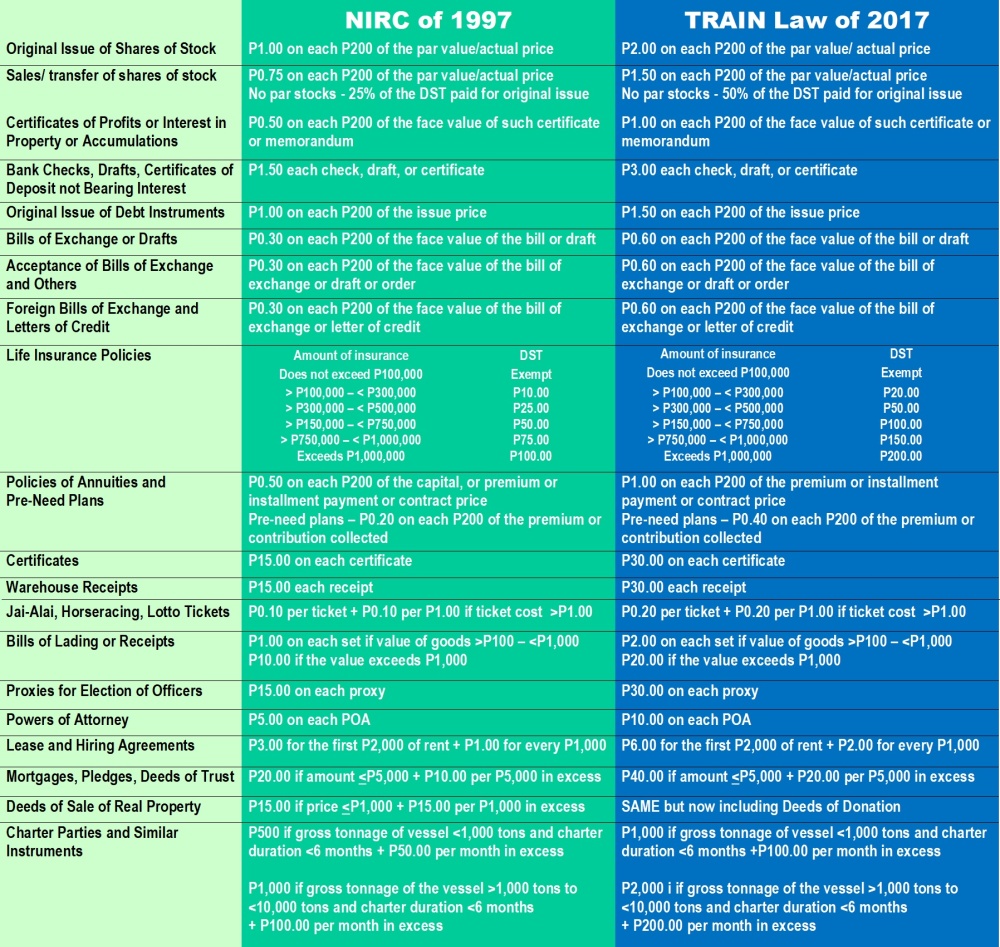

- Documentary stamp taxes [Sections 174, 175, 177, 178, 179, 180, 181, 182, 183, 186, 188, 189, 190, 191, 192, 193, 194, 195, 196 and 197 as amended]

4). Withdrawal of the Preferential Income Tax Rates of Non-Resident Aliens Employed in RHQs/ROHQs of MNCs, OBUs, and PSCs:

There will no longer be a 15% preferential tax rate on the gross income of alien individuals employed by RAHQs/ ROHQs of MNCs, OBUs, and PSCs registered with the SEC beginning January 1, 2018.

*The provision maintaining the special tax rate was vetoed by President Duterte. Affected employees are those working in the BPO industry like call centers.

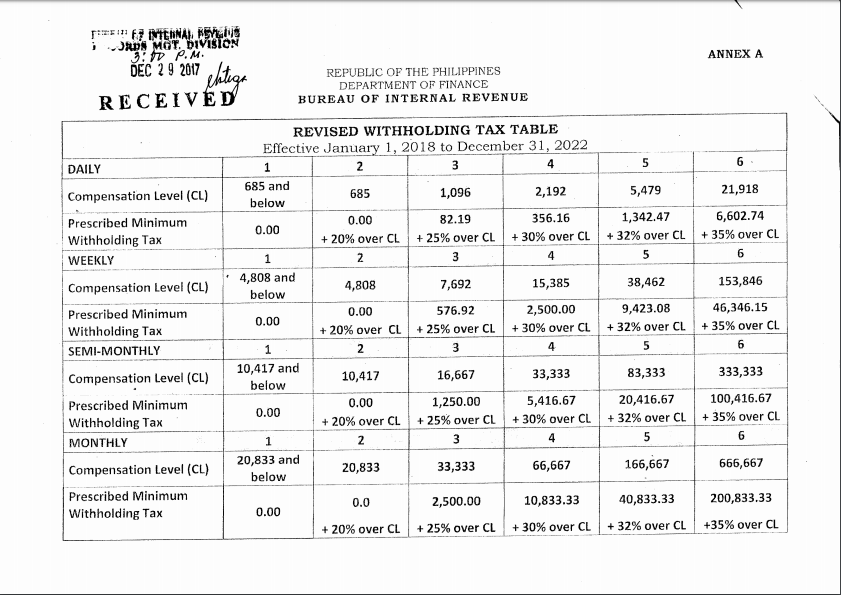

5). Lowering of Withholding Tax Rates:

WHT rates on income will be reduced to not less than 1% to not more than 15% of the income payment starting January 1, 2019. WHT is currently not less than 1% to not more than 32% [Section 57(B)] and the BIR has already updated the rates to reflect the income tax changes under TRAIN.

BIR RMC 1-2018 prescribes the withholding rate for Self-employed lndividuals or Professionals at 8% for the following income payments:

- Professional fees, talent fees, commissions, etc. for services rendered by individuals;

- lncome distribution to beneficiaries of Estates and Trusts;

- lncome Payment to certain brokers and agents;

- lncome Payments to partners of general professional partnership;

- Professional fees paid to medical practitioners; and

- Commission of independent and/or exclusive sales representatives, and marketing agents of companies.

6). Elimination of Personal and Additional Exemptions:

- For individual taxpayers, there will be no more personal exemptions of P50,000 per individual and additional exemptions of P25,000 each for four dependents (Section 35 has been repealed) and no more deduction of P2,400 for PPHHI or Premium Payment for Health and/or Hospitalization Insurance [Section 34 as amended].

- Likewise, estates and trusts are no longer entitled to the P20,000 exemption (Section 62 has been repealed).

7). Availment of OSD by GPPs:

- A general professional partnership and the partners comprising it may avail of the OSD only once, either by the general professional partnership or the partners comprising the partnership [Section 34 (L) as amended].

8). Higher Ceiling Amount for Benefits Excluded in the Computation of Gross Income:

- The amount of gross benefits (13th month pay, allowances, bonuses, and other benefits) received by public and private sector employees excluded from gross income (i.e. not taxable) is increased up to the maximum amount of P90,000 from the previous ceiling of P82,500. [Section 32(B)(7)(e) as amended].

9). Specific Contents and Time for Filing of Returns:

- Tax returns of individuals and corporations can be filed in paper or electronic form and must contain the required information under TRAIN. [Section 51(A)(5) and Section 52(A) as amended].

- Update on exemptions from the requirement of filing income tax returns (ITRs):

-

- Individuals whose taxable income does not exceed P250,000 are not required to file income tax returns provided the individual is not engaged in business or practice of profession [Section 51(A)(2)(a) as amended].

- Pure compensation income earners working for only one employer regardless of the amount of income (even when exceeding the exempt income), provided the income tax has been correctly withheld [Section 51-A].

10). New Period for Payment and Filing of Returns:

- Installment payment for taxes – First installment payment shall be at the time the return is filed and the second installment on or before October 15 following the close of the calendar year (previously July 15 following the close of the calendar year) [Section 56(A)(2)].

- Return for both final and creditable withholding taxes must be filed not later than the last day of the month following the close of the quarter during which the withholding was made. (Previously FWT return filed within twenty-five (25) days from the close of each calendar quarter while CWT return filed the last day of the month following the close of the quarter during which withholding was made [Section 58(A)].

- Individual ITRs now filed on or before May 15. Schedule of payment is accordingly changed to: May 15, August 15, November 15, May 15 of the following calendar year [Section 74 as amended].

- Estate tax returns now filed within 1 year, no longer 6 months, from the decedent’s death [Section 90(B)].

- VAT Return and Payment – Beginning January 1, 2023, the filing and payment for VAT shall be within twenty-five (25) days following the close of each taxable quarter. Payment of VAT until then remains monthly [Section 114(A)].

11). New Rules on VAT:

- VAT zero-rated transactions have been minimized with a view to the future elimination of the zero-rating of certain export sales [Section 108(B) as amended].

- Sale of electricity and transmission by any entity including electric cooperatives now VATable [Section 108(A) as amended].

- New VAT threshold amount for certain transactions [Section 109(P),(Q),(BB) as amended].

- Addition of five more VAT exempt transactions [Section 109(W),(X),(Y), (Z), (AA) as amended].

- Amortization of the input VAT allowed only until December 31, 2021 after which taxpayers with unutilized input VAT on capital goods purchased or imported can only apply the same as scheduled until fully utilized [Section 110(A)(2)(b) as amended].

- Action by the CIR or the processing time on applications for refund of input tax credits now for a shorter period of ninety days from submission of official receipts or invoices and other supporting documents [Section 112(C) as amended] and deliberate inaction by the BIR is punishable by fine, imprisonment and perpetual disqualification to hold office, vote or participate in elections [Section 269(j)].

- VAT withholding will shift from final withholding to creditable withholding beginning January 1, 2021 [Section 114(C) as amended]

12). New Receipts and Invoicing Requirements:

- Mandatory issuance of receipts and invoices for sales valued at not less than P100 (previously only P25.00) by all persons liable for internal revenue taxes.

- Electronic receipts will be required from taxpayers engaged in e-commerce and taxpayers under the Large Taxpayers Service as soon as BIR sets up the Electronic Sales Reporting System within 5 years from the effectivity of TRAIN [Section 237 as amended].

13). New Rule on Deficiency and Delinquency Interest:

- Interest on unpaid taxes no longer 20% per annum but “double the legal interest rate for loans or forbearance of any money in the absence of an express stipulation as set by the BSP” and deficiency and the delinquency interest cannot be imposed simultaneously [Section 249(A) as amended]

- The reckoning period for assessment of deficiency interest is from the date prescribed for its payment until the full payment thereof, or upon issuance of a notice and demand by the CIR, whichever comes earlier [Section 249(B) as amended].

14). Harsher Penalties for Violations of the Tax Code:

- A fine of not less than P500,000 to not more than P10 Million and imprisonment of not less than 6 years to not more than 10 years for the following violations of the Tax Code:

-

- Tax Evasion [Section 254 as amended]

- Unauthorized printing of receipts or sales or commercial invoices [Section 264(B)(1) as amended]

- Printing of double or multiple sets of invoices or receipts [Section 264(B)(2) as amended]

- Printing of unnumbered receipts or sales or commercial invoices, not bearing the name, business style, Taxpayer Identification Number, and business address of the person or entity [Section 264(B)(3) as amended]

- Printing of other fraudulent receipts or sales or commercial invoices [Section 264(B)(4)]

15). New Offenses or Violations Punishable Under TRAIN:

- Printing of other fraudulent receipts or sales or commercial invoices [Section 264(B)(4)]

- Failure to Transmit Sales Data Entered on Cash Register Machine (CRM)/Point of Sales System (POS) Machines to the BIR’s Electronic Sales Reporting System [Section 264-A]

- Purchase, Use, Possession, Sale, or Offer to Sell, Installment, Transfer, Update, Upgrade, Keeping, or Maintaining of Sales Suppression Devices [Section 264-B]

- Offenses Relating to Fuel Marking [Section 265-A]

- Deliberate failure to act on the application for refunds within the prescribed period provided under Section 112 on VAT input tax credit refunds [Section 269(j)]

16).New Subsections Inserted:

- Section 51-A. Substituted Filing of Income Tax Returns by Employees Receiving Purely Compensation Income

- Section 148-A. Mandatory Marking of All Petroleum Products

- Section 150-A. Non-essential Services

- Section 150-B. Sweetened Beverages

- Section 237-A. Electronic Sales Reporting System

- Section 264-A. Failure to Transmit Sales Data Entered on Cash Register Machine (CRM)/Point of Sales System (POS) Machines to the BIR’s Electronic Sales Reporting System

- Section 264-B. Purchase, Use, Possession, Sale, or Offer to Sell, Installment, Transfer, Update, Upgrade, Keeping, or Maintaining of Sales Suppression Devices

- Section 265-A. Offenses Relating to Fuel Marking

Download Full Text, Provision-by-Provision Comparison of the NIRC and TRAIN

Revamped Income Taxation

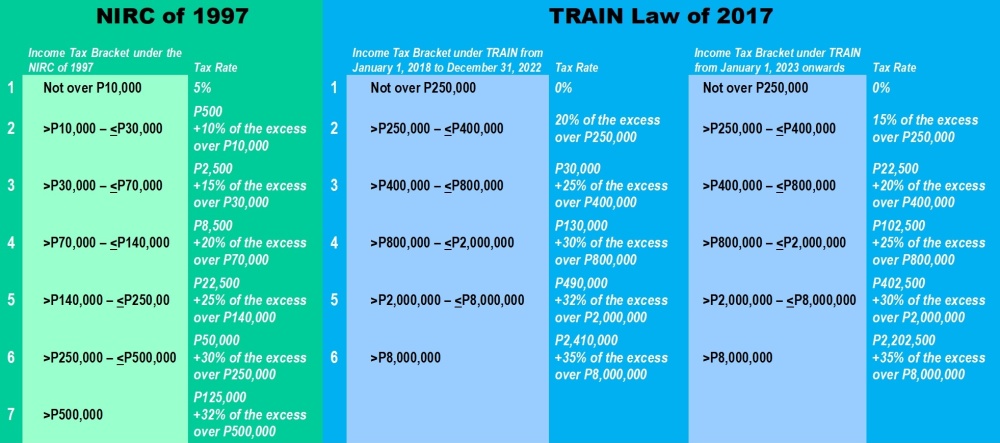

New Tax Brackets and Tax Rates for Individual Taxpayers

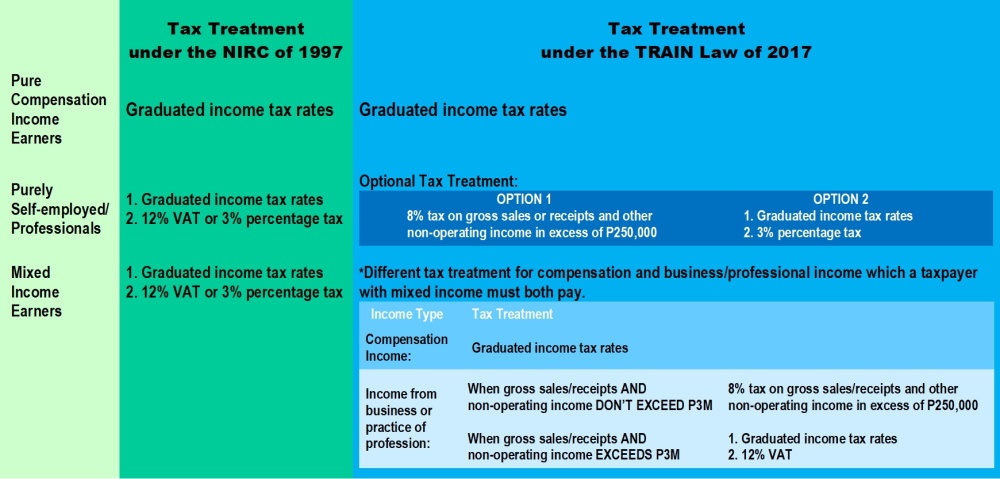

The most drastic reform are the new graduated income tax rates prescribed by TRAIN and the introduction of optional tax treatment for individual taxpayers who are self-employed or are earning income from business or practice of their profession.

Purely self-employed taxpayers or professionals can avail of the 8% tax rate for income they earn in excess of their first P250,000 exempt income rather than pay for 3% percentage tax.

Those with mixed income pay income tax for compensation income and either 8% or the graduated income tax and VAT on their other income.

The graduated income tax schedule is down to six tax brackets from the original seven brackets. There are two waves to the tax reform, the first wave took effect last January 1, 2018 and the second on January 1, 2023 with the second wave imposing lower tax rates on income.

The exempt income threshold has been increased to P250,000 unlike before TRAIN wherein only minimum wage earners or those earning P100,000 annually were exempt from income taxes. On the other hand, the highest tax bracket for income exceeding P8 Million has been increased from 32% to 35%.

Tax on Passive Income

There are two changes on the final income taxes on passive income:

- The tax rate for interest income earned by resident taxpayers and domestic corporations from their foreign currency deposit accounts is now subject to 15% final tax from the previous 7.5%.

- Net capital gains realized from the sale of shares of stock in a domestic corporation not traded in the Stock Exchange taxed at a uniform rate of 15% without regard to the amount of the net gain. The previous tax treatment was 5% for the first P100,000 net gain and 10% on the amount in excess of P100,000.

Stock Transaction Tax Now 6/10 of 1% of GSP

It is now more costly on stock traders as the sale, barter, exchange, or other disposition of shares of stock listed and traded through the local stock exchange are now taxable at the rate of six-tenths of one percent (6/10 of 1% or 0.6 of 1%) of the gross selling price or gross value in money instead of one-half of one percent (1/2 of 1% or 0.5 of 1%).

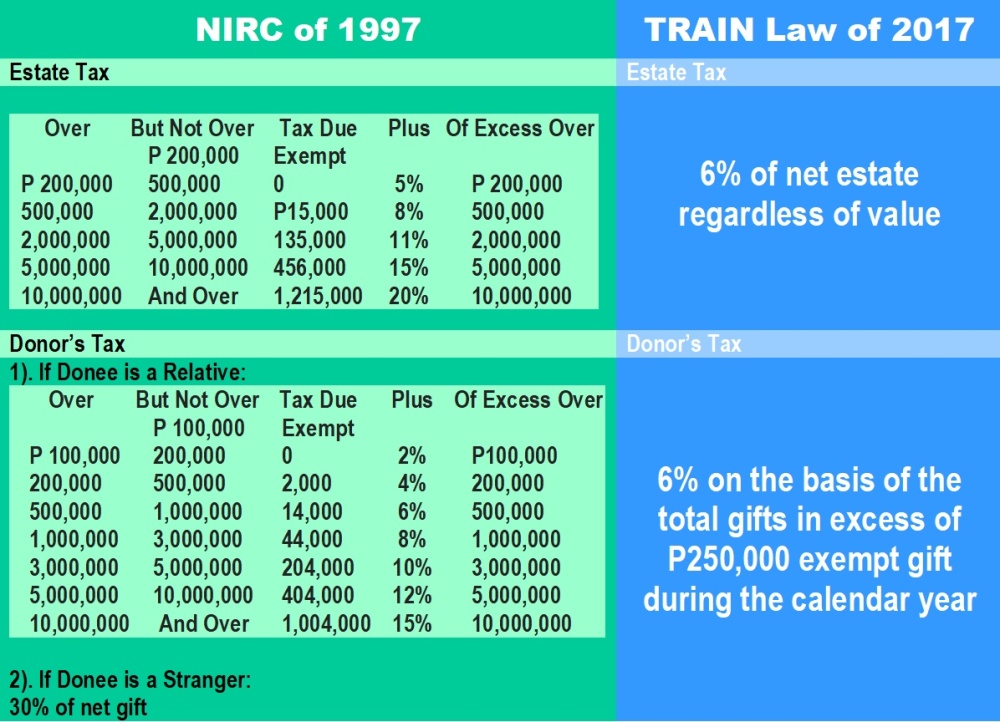

Reform on Transfer Taxes

The reform on estate and donor’s tax is vastly favorable to the very few wealthy segment of the populace with properties to transfer. The graduated tax schedule for estate and donor’s taxes has been discarded and replaced with the uniform flat rate of 6%. A P10 Million net estate that would have owed P1.215 Million in taxes under the NIRC is now only liable for a tax of P600,000!

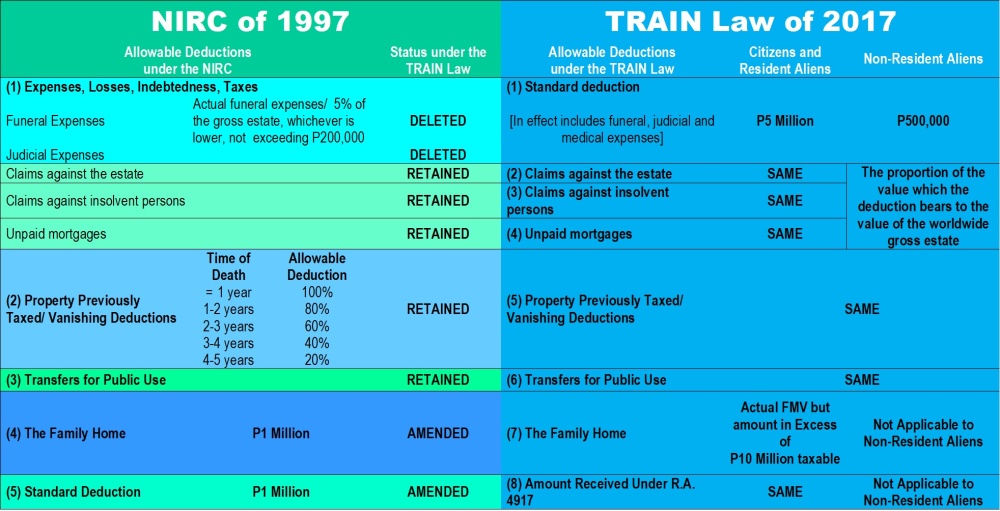

Allowable Deductions from the Estate

TRAIN eliminated the distinction between ordinary and special deductions and allows only eight deductions from the estate. Also deleted are the deductions for funeral, judicial and medical expenses which has been lumped altogether into a standard deduction of P5 Million. Hence, estates valued below P5 Million will not yield any tax due under the TRAIN Law. Where before TRAIN only P1 Million can be claimed as a deduction for the family home, the law now allows a deduction of P10 Million and only the amount in excess is subject to estate tax.

Other Changes in Estate Taxation

- Notice of Death is no longer required (Section 89 has been repealed)

- Estate Tax Returns must be filed and the tax due therefrom paid within 1 year (previously within 6 months) from the decedent’s death [Sections 90(B) and 91(A) as amended].

- Estates with gross value of P5 Million (previously P2 Million) must file an estate tax return supported with a statement duly certified by a CPA [Section 90 as amended].

- Other than extension of time for payment, estate taxes may now be paid in installment within two (2) years from the statutory date for its payment without civil penalty and interest when the estate has insufficient cash [Section 91(C) as amended].

- Withdrawal from the bank account of the decedent is already allowed but subject to FWT of 6% (withdrawal of more than P20,000 used to be prohibited without certification from the CIR that taxes have been paid) [Section 97 as amended].

Donor’s Tax

The amount of exempt gifts has been increased to P250,000 (previously P100,000 only) per calendar year. However, dowries of P10,000 given to one’s children on account of marriage are no longer exempt gifts.

Value-Added Tax

Zero-Rated Transactions Limited in TRAIN

TRAIN no longer considers foreign currency denominated sales as zero-rated sale of goods, only retaining export sales and sales to persons and entities exempt under special law or international agreements.

Sale and delivery of goods as well as rendition of services to PEZA and TIEZA registered enterprises which were proposed to be included as zero-rated sales in the enrolled bill was vetoed by President Duterte while sale of gold to the BSP is no longer a zero-rated transaction but still VAT-exempt.

However, the government now has leeway to subject to 12% VAT certain kinds of export sales upon the happening of the two conditions:

- The successful establishment and implementation of an enhanced VAT refund system that grants refunds of creditable input tax within ninety (90) days from the filing of the VAT refund application with the Bureau

- All pending VAT refund claims as of December 31, 2017 shall be fully paid in cash by December 31, 2019 [Section 106 as amended]

Transactions that may lose the zero-rating are:

- Sale of raw/ packaging materials to a nonresident buyer for delivery to a resident local export-oriented enterprise (EOE) to be used in manufacturing, processing, packing or repacking in the Philippines of the said buyer’s goods and paid for in acceptable foreign currency and accounted for in accordance with the rules and regulations of the BSP;

- Sale of raw materials or packaging materials to an EOE whose export sales 70% of total annual production;

- Those considered export sales under Omnibus Investment Code and other special laws;

- Processing, manufacturing or repacking goods for other persons doing business outside the Philippines which goods are subsequently exported, where the services are paid for in acceptable foreign currency and accounted for in accordance with the rules and regulations of the BSP

- Services performed by subcontractors and/or contractors in processing, converting, of manufacturing goods for an enterprise whose export sales exceed 70% of total annual production.

Expanded VATable Sale of Services

TRAIN subjects to VAT the sale of electricity by generation companies, transmission by any entity, and distribution companies including electric cooperatives.

Thus, transmission by the National Grid Corporation of the Philippines (NGCP) is no longer exempt from VAT. The increase in wheeling charges for the services of the NGCP in the transmission of electricity from power plants to distribution facilities due to the removal of the exemption and, together with the increase in excise taxes on coal which is the main source of fossil fuel by power generation companies, will result in higher cost of electricity.

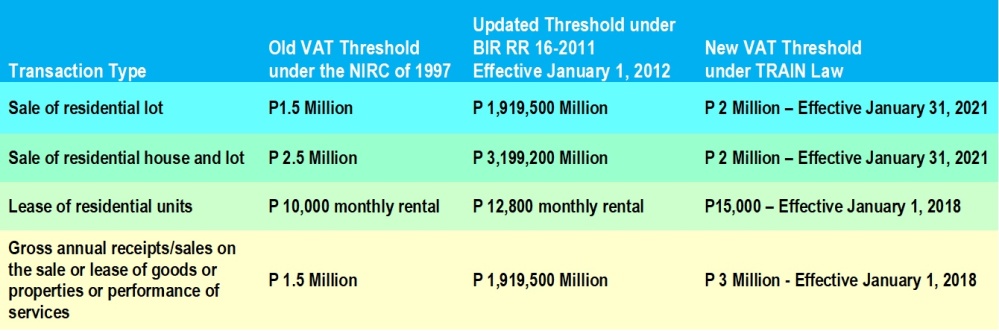

New VAT Thresholds

TRAIN imposes P3 Million as the new threshold amount for businesses to be subject to VAT, if the annual gross sales or receipt does not exceed P3 Million, the taxpayer is liable only for the 3% percentage tax.

The threshold for VAT Exemption in the sale of real properties not primarily held for sale or business or capital assets sold in isolated transactions like sale of residential lot or house and lot including the lease of residential units with monthly rental has been updated by TRAIN:

Additional VAT Exempt Transactions

TRAIN added five more exempt sales:

- Sale or lease of goods and services to senior citizens and persons with disability

- Transfer of property pursuant to Section 40(C)(2) of the NIRC, as amended

- Association dues, membership fees, and other assessments and charges collected by homeowners associations and condominium corporations;

- Sale of gold to the BSP

- Sale of drugs and medicines prescribed for diabetes, high cholesterol, and hypertension beginning January 1, 2019

Excise Taxes

Expanded Coverage of Excise Taxes

Sale of services performed in the Philippines subject to ad valorem tax under TRAIN, specifically sale of non-essential services like invasive cosmetic procedures, surgeries, and body enhancements taxed at 5% of the gross receipts from such procedures. Doctors or clinics are expected to collect the levy from their patients, which would be later on remitted by the doctors in what is called reverse withholding.

Sweetened beverages and petroleum coke are now excisable articles while the existing taxable articles now have higher excise tax rates:

- Cigarettes Packed by Hand and Packed by Machine

- Refined and manufactured mineral oils and motor fuels

- Automobiles

- Mineral products

Excise Tax on Cigarettes

The rate adjustment is implemented by RR No. 3-2018 amending RR No. 17-2012.

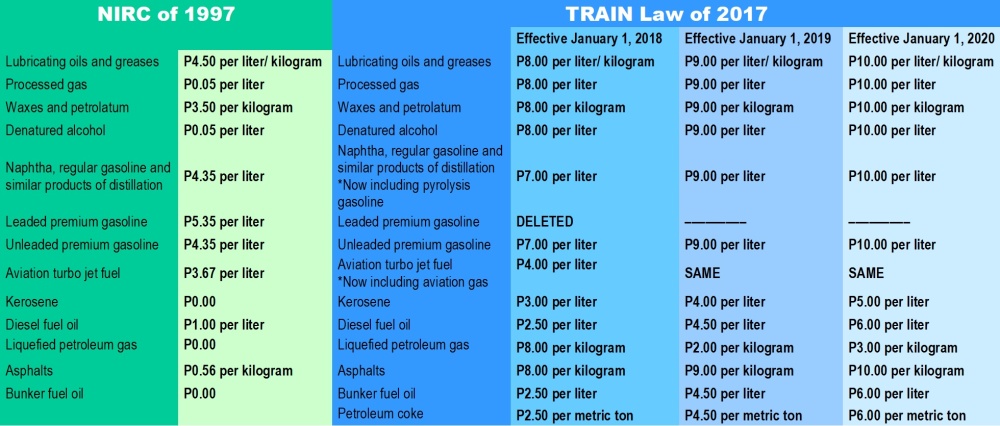

Excise Tax on Mineral Oils and Motor Fuels

The increase of the excise taxes on motor fuels and petroleum product is the most austere for all taxpayers as the zero-rating of kerosene, LPG and bunker fuel oil have been withdrawn with three scheduled waves of rate hikes.

To alleviate the ill-effects of the regressive tax on the poor, TRAIN will provide social benefits card to qualified beneficiaries with benefits such as unconditional cash transfer (P200.00 per month for the first year which increases to P300.00 for the second and third year) and fuel vouchers to qualified franchise holders of PUJs as well as 10% fare discount from all public utility vehicles and 10% discount on the purchase of NFA rice for up to a maximum of 20 kilos per month. The implementation of the scheduled increase will also be suspended when the average Dubai crude oil price for three months prior to the scheduled increase of the month reaches or exceeds USD 80 per barrel.

However, the social benefits program will last for the first three years of TRAIN and the suspension of the increase in excise tax will not result in any reduction of the excise tax being imposed at the time of the suspension.

BIR has already issued RR No. 2-2018 implementing the revised rates.

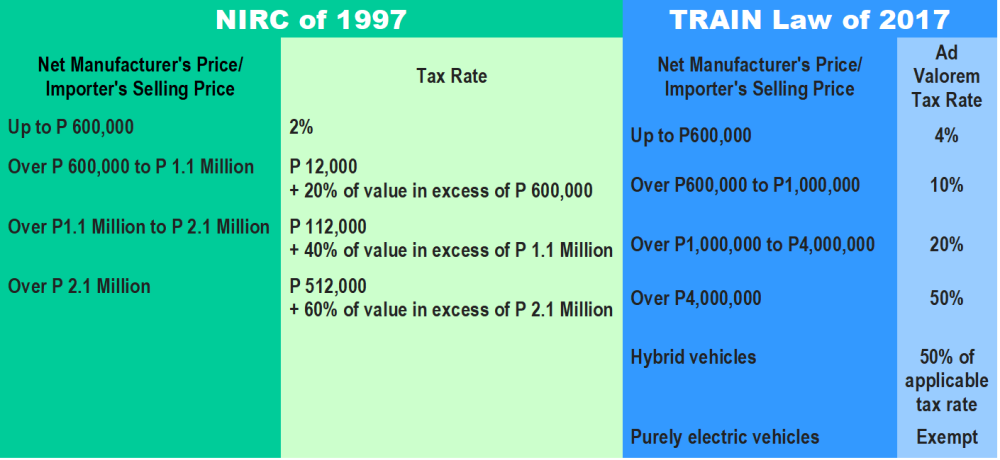

Excise Tax on Automobiles

The TRAIN law has adjusted the tax bracket and tax rates for the ad valorem tax on automobiles based on the manufacturing or selling price but hybrid vehicles enjoy preferential rates of 50% of the applicable tax while purely electric vehicles and pick-ups are exempt altogether. Excluded from the definition of taxable automobiles are buses, trucks, cargo vans, jeepneys/jeepney substitutes, single cab chassis and special-purpose vehicles.

The BIR has issued RR No. 5-2018 providing for the revised tax rates of excise tax on automobiles. RR No. 5-2018 amends the existing rules on excise taxes on automobiles, RR No. 22-2003.

In RR No. 5-2018, for tax exemption purposes, the Department of Energy is tasked to determine whether the automobiles are hybrid or purely electric vehicles prior to its removal from the manufacturing plant or customs custody.

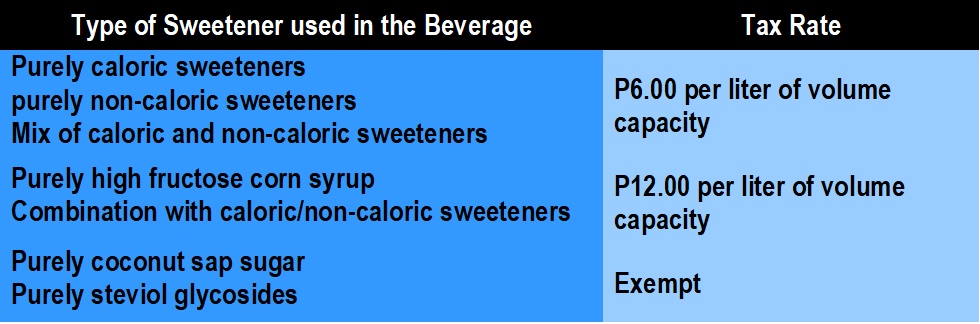

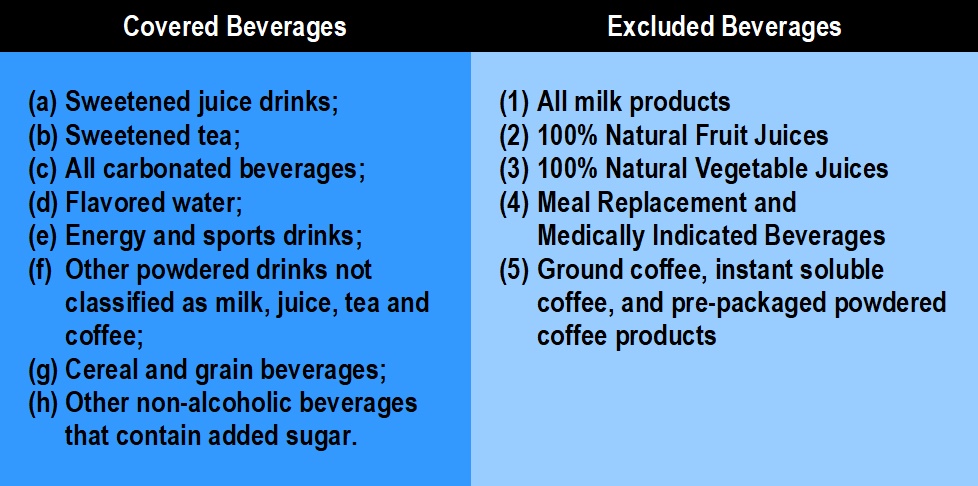

Sweetened Beverage Tax

Sweetened beverages using caloric, non-caloric sweeteners or high fructose corn syrup are subject to excise tax of either P6.00 per liter or P12.00 per liter.

Beverages using syrups prepared from sucrose, fructose and glucose and artificial sweeteners like aspartame, sucralose, saccharin, acesulfame, potassium, neotame, cyclamates are covered by TRAIN while those without added sugar or sweetener are excluded except coffee and milk even if pre-packaged and ready to drink with sweeteners.

Excise Tax on Mineral Products

RR No. 1-2018 is the BIR issuance implementing the new rates.

Documentary Stamp Taxes Doubles

All the existing DST rates have doubled except for DST on the sale or conveyance of real property which has not changed except that deeds of donation are now subject to the same DST rate. But exempt donations are likewise exempt from DST. DST rates have increased by a 100% except for DST on the original issuance of debt instruments which increased only by 50%.

The DST Rate Adjustment is implemented by RR No. 4-2018.

My 2¢ on TRAIN

I wish the TRAIN Law was the Tax Code I had to study for the bar. The copious notes I made and the diagrams I drew to mind-map labyrinthine tax concepts and remedies of the previous Tax Code are now obsolete! Although I appreciate the new law for making tax a less daunting subject to study, I grieve over its real life application.

The TRAIN Law revamped the National Internal Revenue Code, tax rates are uniform and simplified albeit with noticeable inequitable effects. Equality or theoretical justice has been disregarded in favor of administrative feasibility in the collection of taxes by increasing and widening the scope of excise taxes, an indiscriminate kind of tax which, although paid by manufacturers and sellers, end-up bundled with the purchase price of goods and services and ultimately burdens end-consumers. Relief felt by salaried workers from the expanded exemption from income tax will sadly be short-lived as the market prices of goods and services shoot up…what the government is giving away with one hand is being taken away by the other…lost revenues from income taxes will have to be recouped from the excise tax collection.

But on a less political note, I also appreciate the rationale of some of the tax measures. The imposition of excise taxes on cigarettes, automobiles, cosmetic surgeries and sweetened beverages are for laudable purposes. Tax cigarettes and sweetened beverages because: health. Tax automobiles because: traffic. Tax cosmetic surgeries because: vanity is against public policy.

*Updated January 27, 2018 with new revenue regulations issued by the BIR related to the TRAIN.

Hi there My brother suggested I might like this website. He was entirely right. This post actually made my day. You can not imagine just how much time I had spent for this info! vielen dank

LikeLike

TRAIN law is good for us low income filipinos…we do not even need to pay personal income tax if our yearly income does not exceed 250,000 pesos…

LikeLike